This Week in Markets - July 5: The Quiet Week That Decides if the Chip Flush Is Over

Jobs came in soft, Korea got margin-called mid-rally, and now a light calendar hands the tape to the Fed minutes, Samsung, and Delta.

Welcome back to another weekly market prep with The Dividend Journal! If this is your first time here, great timing. This newsletter is your one stop shop to stay ahead of the market and step into the week fully prepared.

New format this week: I’m walking you through the week the way I actually prepare for it, day by day, with what each event means and what I’m doing about it. Let’s get into it.

⚡ Last Week Overview

The jobs report missed badly. June payrolls came in at 57,000 vs 115,000 expected, and April/May were revised down a combined 74,000. Unemployment ticked DOWN to 4.2%, but only because participation fell to its lowest since March 2021 (CNBC). Soft enough to quiet the rate-hike conversation, not soft enough to scream recession (Kiplinger).

The rotation went vertical. The Dow ripped nearly 600 points to a record close of 52,900 on Wednesday while the Nasdaq slid, dragged by chips (CNBC). By Thursday’s holiday-shortened close the S&P sat at 7,483 and the Nasdaq at 25,833, both green on the week despite the chip carnage underneath (TheStreet).

Chips took the hit. A BofA “bubble” call, reports of Anthropic building its own AI chips with Samsung, and SK Hynix slowing HBM expansion knocked the Philadelphia Semiconductor Index roughly 12% over two sessions, with Micron down 13% in a day (Axios, KuCoin).

Korea got margin-called. The KOSPI fell 6.4% within minutes of Thursday’s open, broke below 8,000, and tripped its third emergency halt in two weeks (Investing.com). Korean retail margin debt is at a record 38 trillion won, and Samsung plus SK Hynix are 53% of the index (Korea Herald). I broke down the full leverage chain in Saturday’s video if you missed it.

🃏 The Wild Card: A Leveraged Unwind Meets a Silent Calendar

This week is light on data, which cuts both ways. Nothing on the calendar is big enough to rescue the tape, and nothing is big enough to break it either, so the chip flush gets to resolve on its own supply and demand (Schwab). The open question: is the forced selling out of Korea done, or does record margin debt have another leg of liquidation in it?

The path higher is straightforward. The deleveraging exhausts itself, Samsung’s preliminary numbers land firm, and Wednesday’s minutes read calmer than feared after the jobs miss. In that world the oversold chip names bounce off support and the “healthy flush” read wins. Honestly, the more likely outcome is quieter than that: with no catalyst big enough to force a resolution, the tape chops in a range on thin summer liquidity while everyone waits for CPI and bank earnings the following week.

In all honesty, memory names don't look like they have built in a blow off the top quite yet. Names like MU 0.00%↑ are still priced as under valued given the backlog they have.

What I’m guarding against is the other tail. If the minutes reveal the committee was closer to a hike than the market wants to believe, or Samsung guides soft and confirms the memory demand doubts, the calendar offers nothing to catch the knife. With Korean margin debt still at records, weakness forces more selling, and the second leg down in chips arrives before any data can help.

🗓️ The Week, Day by Day

Monday, July 6: Markets reopen from the long weekend to the first full session since the jobs miss. No major US data. The tell comes overnight: Seoul trades Sunday night our time, and whether the KOSPI stabilizes or trips halt number four sets the tone for chips at our open. Watch whether the semis hold last week’s lows.

Tuesday, July 7: Quiet on the US calendar. The one to watch for is Samsung’s preliminary Q2 numbers, which typically drop in the first week of July (Samsung IR). It’s the first hard datapoint on whether memory demand justifies the run Korea leveraged itself into, and every US memory name trades off it.

Wednesday, July 8: The main event. FOMC minutes from Kevin Warsh’s first meeting as chair drop at 2pm ET (Kiplinger). Warsh skipped the dot plot, so these minutes are the closest thing we get to his playbook. The question isn’t what they decided, it’s how close the committee actually was to hiking BEFORE payrolls came in soft. Consumer credit, wholesale inventories, and crude inventories land the same day.

Thursday, July 9: Weekly jobless claims and continuing claims. After a 57k payrolls print, the weekly claims data graduates from background noise to the live pulse of the labor market. A jump in continuing claims would feed the slowdown narrative; steady claims would support the “cooling, not cracking” read.

Friday, July 10: Delta reports before the open and unofficially opens Q2 earnings season (Yahoo Finance). Consensus sees EPS down about 31% year over year. Beyond the airline itself, it’s the first real read on whether the consumer showed up for summer.

And then the calendar loads up: CPI lands Tuesday July 14, PPI on the 15th, the big banks kick off earnings the same week, and TSMC reports July 16 (TSMC). This week is the deep breath before all of that.

📈 Market Update

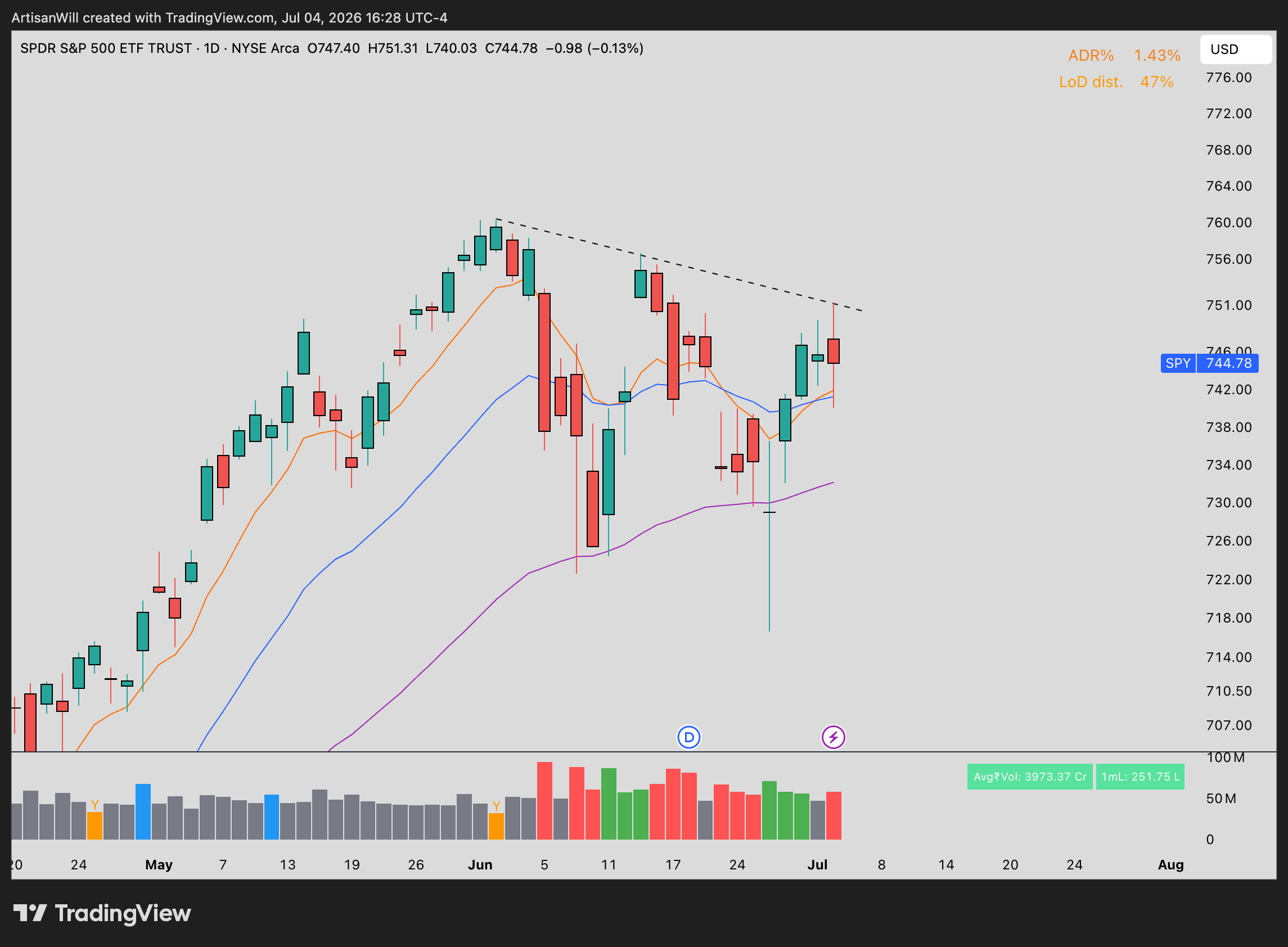

SPY 0.00%↑- Along with the Dow, the S&P is a lot stronger than tech and the divergence is largely driven by chip stocks pulling back. The flag is tighter and clearer on SPY 0.00%↑ with price still above all EMAs.

Financials like V 0.00%↑ and MA 0.00%↑ were really strong as of Thursday close as well as healthcare names like ABBV 0.00%↑, MRK 0.00%↑, and LLY 0.00%↑.

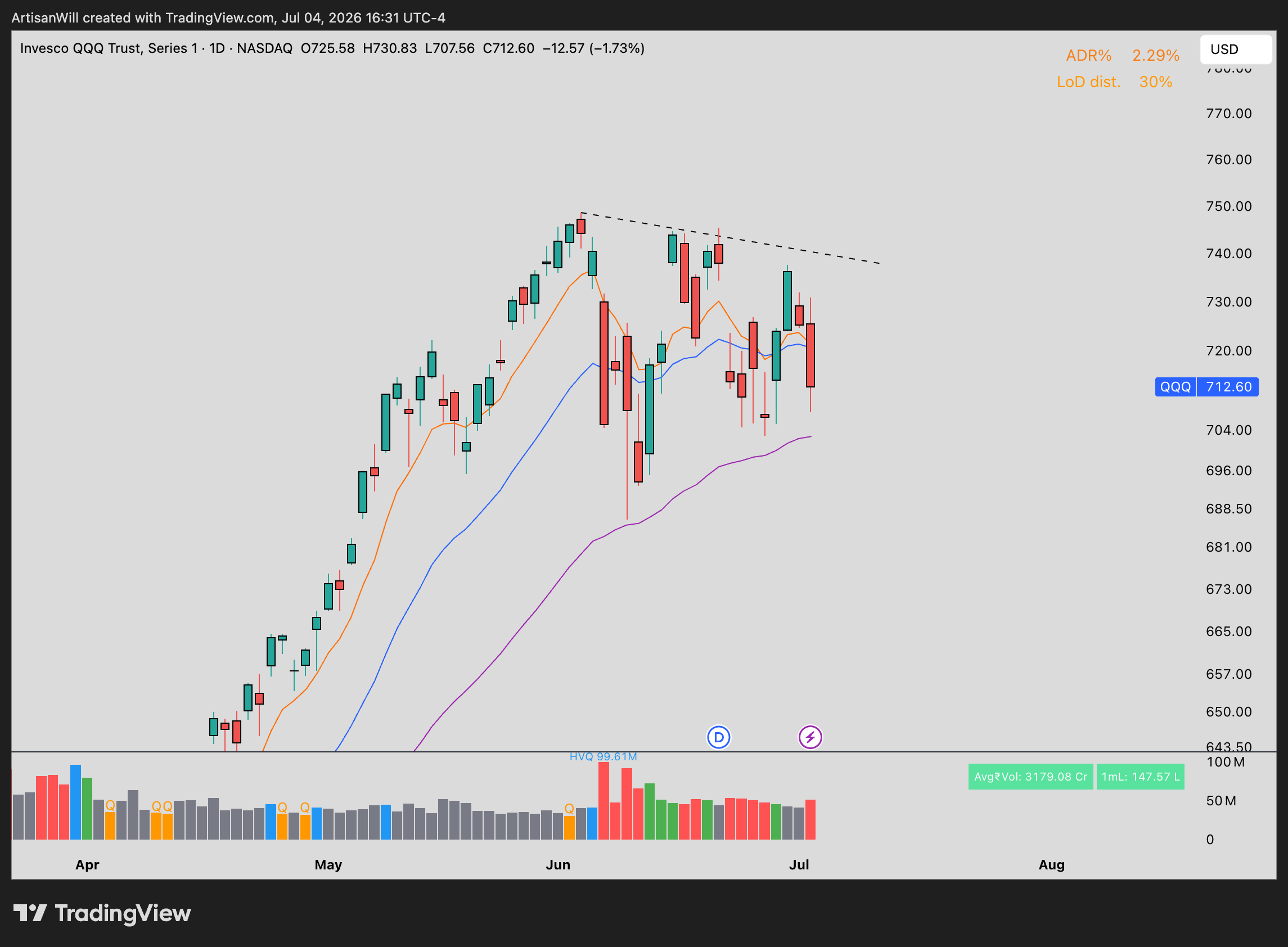

QQQ 0.00%↑- Tech is a lot weaker and revisiting the daily 50EMA. For an uptrend and for this flag to be valid, this is the spot for price to bounce. So I’m looking this week to see if there is another rotation out of financials and healthcare back into tech.

Regardless, a lot of tech name charts have been broken and need some more time to become structurally tradable again.

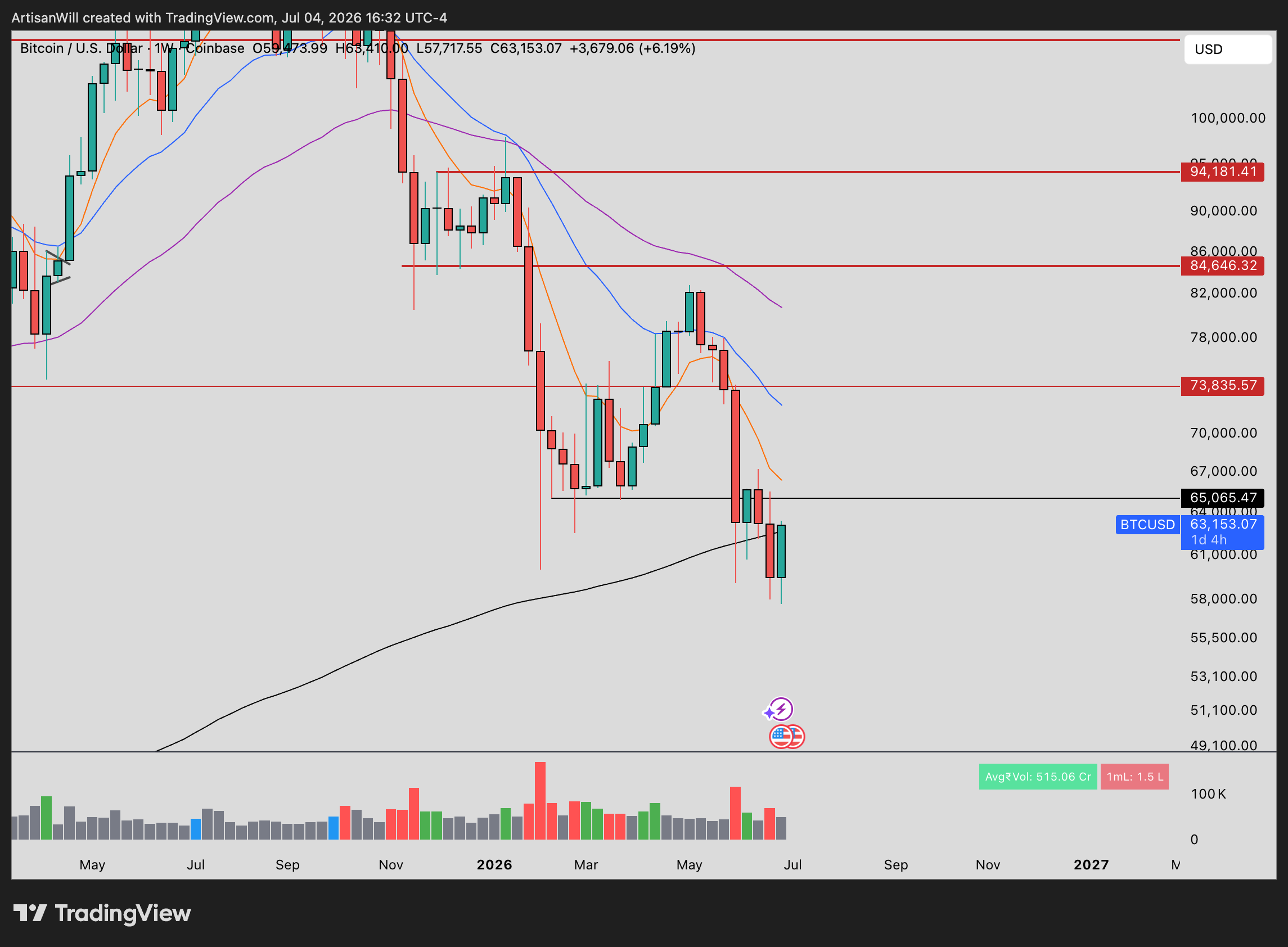

Bitcoin - Meanwhile, we’re seeing a rotation out of chip stocks into crypto for this weekend. Price is currently working on a weekly hammer, which is a good start for potential bottoming price action.

The bottoming is expected around September to October of this year but this current action could be a good precursor.

🔍 What I’m Watching

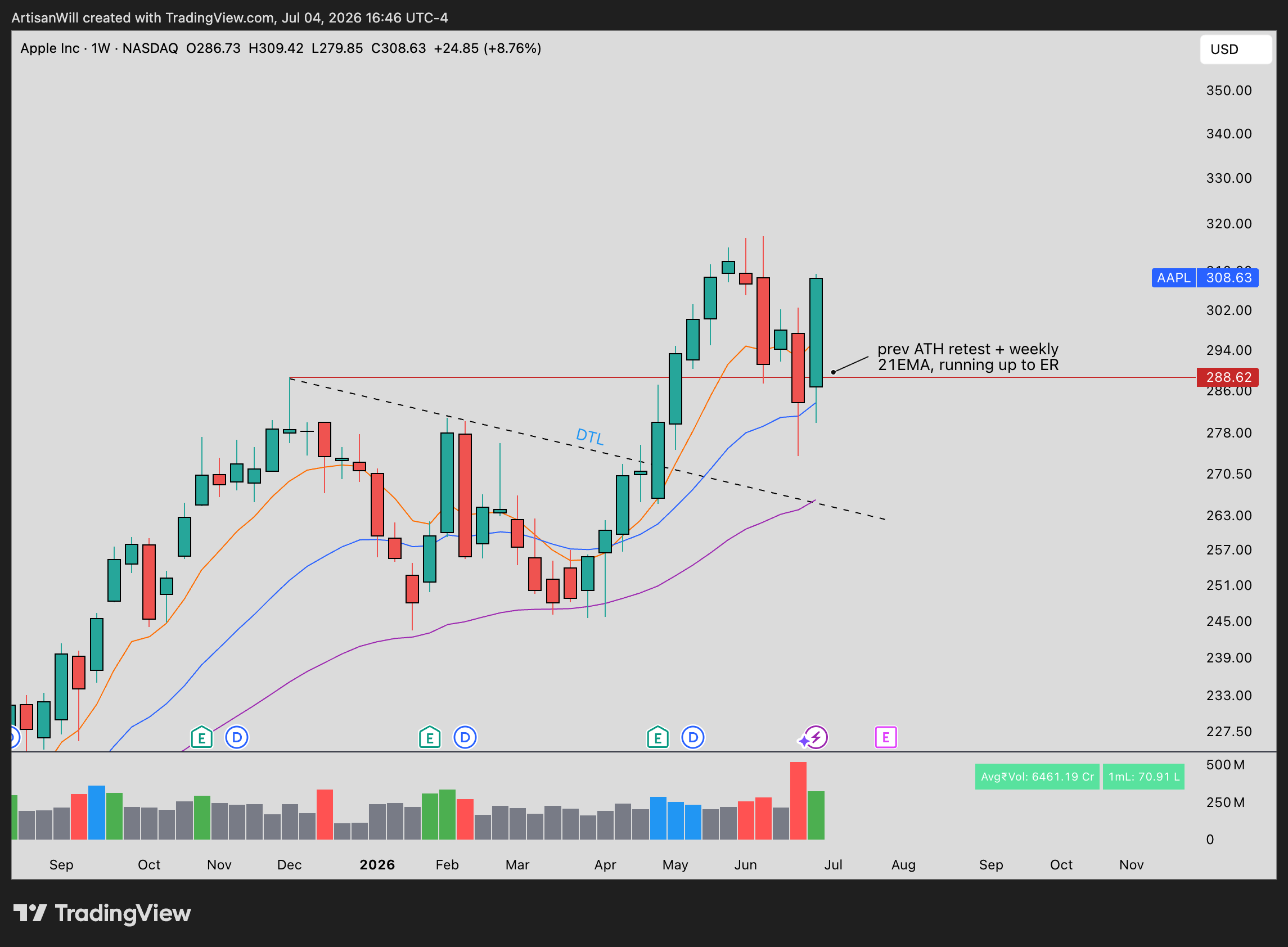

AAPL 0.00%↑ - One of the MAG7 names that has proven to be strong when the rest of the market is a little weaker.

The weekly retest of the 21EMA + previous ATH range is really interesting here as we approach earnings late July. We can definitely see a continuation move to new highs soon here.

Looking for low volume pullbacks to 300 to let the daily EMAs play catch up before the next push up.

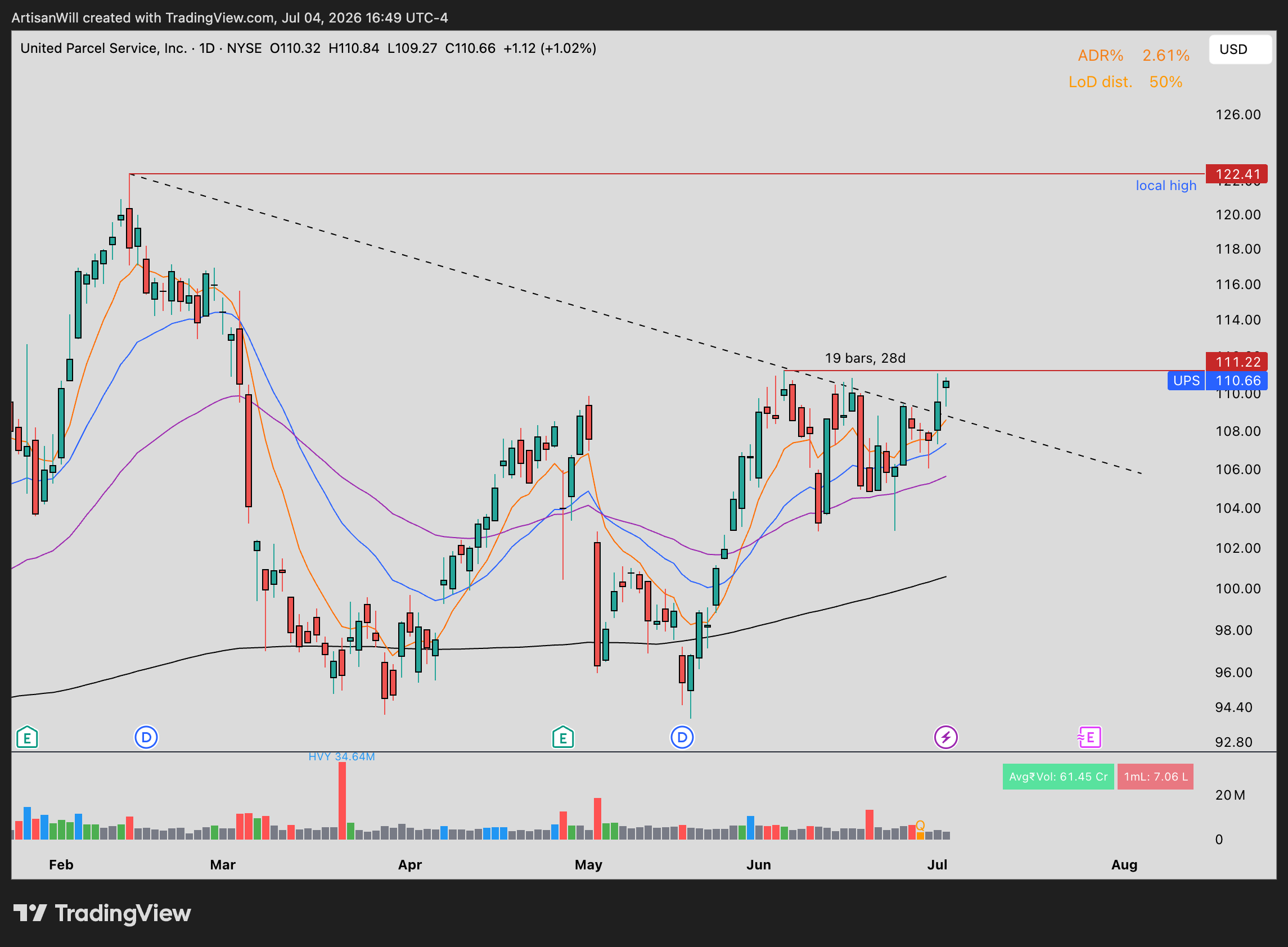

UPS 0.00%↑ - Setting up really nicely for an attempt at a breakout over 111.22 to potentially test the local high at around 122.

The price action here is significant because we are seeing detachment off the EMAs. This indicates momentum beginning to pick up. With names like these, we’ll usually see a huge push one day with high volume and then it drifts upwards afterwards.

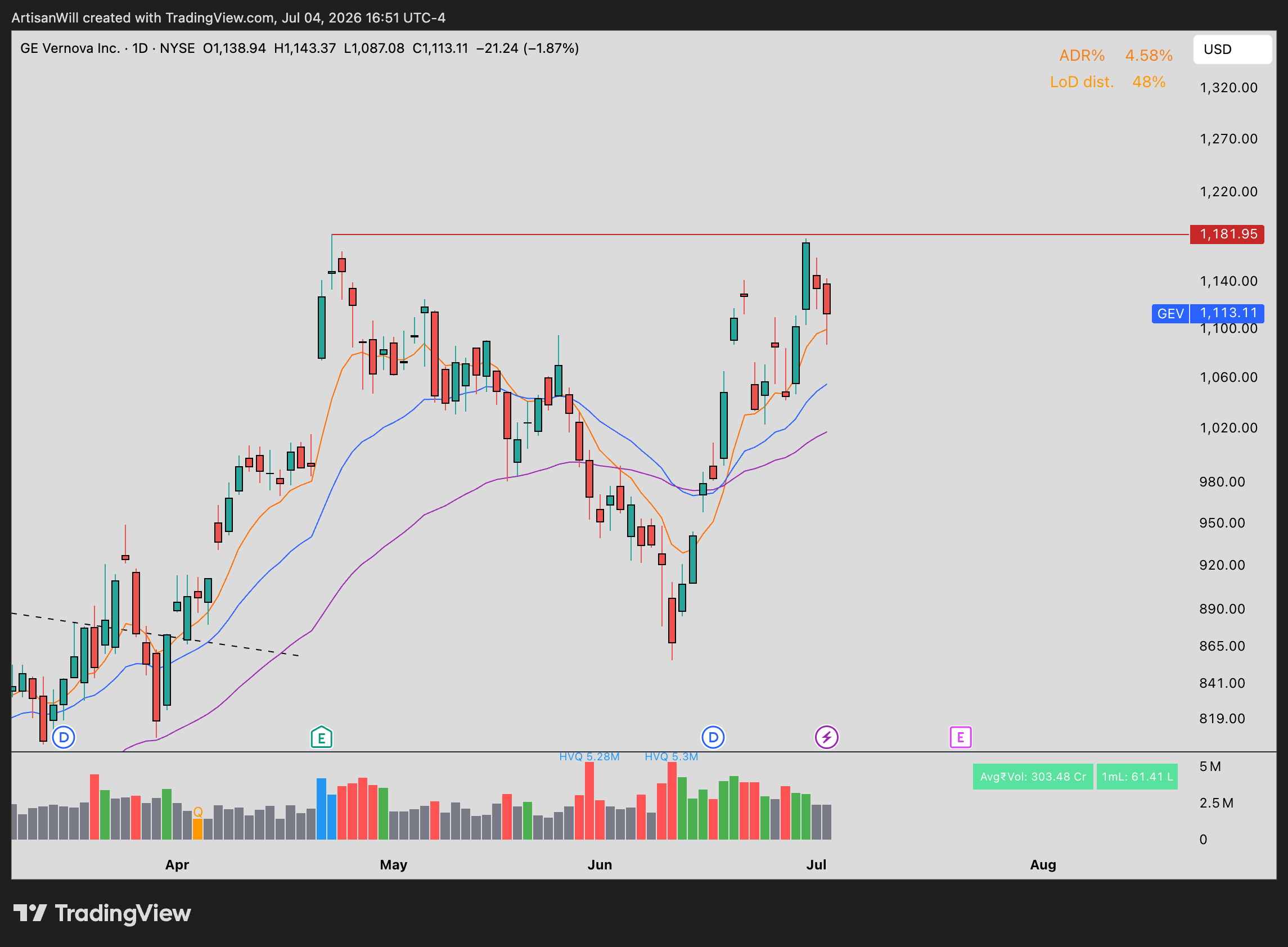

GEV 0.00%↑ - strong energy name with a low volume retracement into daily EMAs. I would love to see price rebound and tighten up near the 1181 base level before we break higher as an earnings run up.

This company has great fundamentals and a sharp growth story, so a run up would not be surprising.

💡 My Take

Everyone wants to know if the AI trade just topped. Wrong question for this week. What broke the chips wasn’t demand, it was positioning: a two stock index doubled on borrowed money, the margin calls hit, and the selling went global. Positioning problems resolve differently than demand problems. They end when the leverage is gone, not when the story changes, and no report this week tells you which day that is. Price tells you. That’s why the levels matter more than the headlines for the next five sessions.

My posture: I said it in Saturday’s video and I’ll say it here, the US memory play does not look like a blow-off top to me yet. But “not a top” is not the same as “buy Monday.” I want to see the semis hold last week’s lows and put in a higher low before I trust a bounce, and I want Samsung’s preliminary numbers to confirm the demand side is intact. If both show up, the oversold names earn the benefit of the doubt. If the lows break with Korean margin debt still at records, I step aside and let the forced sellers finish.

Process over prediction this week: let Monday and Tuesday show you whether the flush is done, treat Wednesday’s minutes as a repricing risk rather than a trade, and keep size small until the levels confirm. The loaded week is the one after this one. The traders who survive the quiet week with their capital and their patience intact get to play it.

See you next week. Trade well.

Will