This Week in Markets - July 12: CPI Walks Into the Warsh Fed's First Test

June inflation lands the same morning the new hawkish Fed chair takes the witness chair, with a September rate hike already most of the way priced.

Welcome back to another weekly market prep with The Dividend Journal! If this is your first time here, great timing. This newsletter is your one stop shop to stay ahead of the market and step into the week fully prepared.

The averages closed out another winning week, with the S&P 500 at 7,575.39 and the Dow at 52,637.01 after setting fresh record highs midweek. But the calm on the surface is hiding the real story. We are now living under a Kevin Warsh Fed, and the market has spent the last month repricing from rate cuts to rate hikes, with futures now placing roughly 70% odds on a September hike.

This is the week that math gets tested. June CPI, June PPI, two days of Warsh testimony, and the banks kicking off earnings season all land inside five sessions. Everything the tape does this week runs through that single question of whether the Fed hikes again.

Let’s get into it.

⚡ Last Week Overview

The big averages won the week, but the small caps stayed home. The S&P 500 rose 0.4% Friday to 7,575.39, the Nasdaq added 0.3% to 26,281.61, and the Dow gained 149.60 points to 52,637.01. The Russell 2000 went the other way, slipping 0.63% to 2,973.79. When large caps make records while small caps lag, that is the market telling you it wants safety and scale, not risk.

Semiconductors were the whole show, in both directions. A gauge of chipmakers sank more than 4.5% midweek on fresh worries about whether AI spending justifies the valuations, then sentiment flipped when SK Hynix soared 13% in its $26.5 billion Nasdaq debut, the largest foreign IPO to date. The AI memory trade is still the market’s pulse.

Rates and oil both leaned against the bulls. The 10-year Treasury yield pushed up to 4.569%, and WTI crude held around $71.91 as tensions in the Strait of Hormuz kept a bid under energy, even after crude’s steep 20.4% drop in June. Higher yields plus firmer oil is the exact cocktail a hawkish Fed does not want to see.

A soft June jobs report was the week’s relief valve. Weak June labor data gave the doves something to point at and eased fears of an imminent hike. That is the crack in the hawkish case, and it is why this week’s inflation prints matter so much.

Bitcoin quietly had its best stretch since spring. Bitcoin traded up to $64,023, gaining about 1.94% and logging its best week since March as inflation breakevens firmed. Crypto is trading like an inflation hedge again, not a risk asset.

🃏 The Wild Card: Does June CPI lock in a September rate hike, or hand the doves an exit?

The single biggest open question this week is whether the data confirms the market’s move toward a September hike or gives it a reason to back off. The calendar could not be more concentrated. June CPI hits Tuesday at 8:30 a.m. ET, and roughly ninety minutes later Kevin Warsh takes his seat in front of the House Financial Services Committee for his first congressional testimony as chair. June PPI and a second day of Warsh testimony follow Wednesday. So the market gets the inflation read and the Fed’s live reaction to it inside the same 48 hours, with no time to look away.

The clean path runs through the headline number. Consensus looks for headline CPI to actually dip 0.1% month over month, trimming the annual rate to about 3.9% as June’s collapse in energy prices flows through. A soft headline is the most likely outcome, and it gives the doves a talking point and lets Warsh sound firm without committing to September. That is the version where yields ease, the record-setting large caps hold, and the small caps finally get some room to breathe. The catch is that the number that actually moves this market is core, not headline, and core is still expected to grind up another 0.3% with the annual trend stuck near 2.9%. A friendly headline sitting on top of sticky core is exactly the setup that lets bulls and bears both claim victory for a day before the real trend reasserts.

The downside tail is a hot core print landing in front of a chair who has already told the world inflation is “too high” and whose colleagues have shifted hard, with nine of eighteen FOMC participants now penciling in at least one hike this year and BofA calling for three hikes to a 4.25% to 4.5% range. If core runs hot and Warsh leans into it under oath, September odds go from likely to near certain, the 10-year pushes higher, and the same mega-cap valuations that led the market up become the ones with the most to lose. That is the scenario to size for even if you do not expect it.

🗓️ The Week Ahead

Tuesday, July 14: The main event. June CPI at 8:30 a.m. ET sets the tone for the whole week, and Warsh testifies before the House Financial Services Committee at 10:00 a.m. right on top of it. Then the banks open earnings season, with JPMorgan Chase, Bank of America, Goldman Sachs, Wells Fargo, and Citigroup all reporting. Watch core CPI over the headline, and inside the banks watch net interest income and loan loss provisions for the real state of the consumer and credit.

Wednesday, July 15: June PPI at 8:30 a.m. ET is the second half of the inflation picture, and Warsh moves over to the Senate Banking Committee at 10:00 a.m. for round two. Earnings from ASML, Johnson & Johnson, Morgan Stanley, and BlackRock fill out the day. Watch PPI for pipeline pressure that feeds future CPI, and watch ASML’s order book as the cleanest signal on whether the AI capex cycle is still accelerating.

Thursday, July 16: A double dose of the consumer with June retail sales and weekly initial jobless claims, both at 8:30 a.m. ET. Then the marquee earnings drop: TSMC, GE Aerospace, UnitedHealth, Abbott, and Netflix, which is expected to post $0.79 per share on revenue up 13.7% to $12.6 billion. Watch retail sales for whether the soft jobs data is bleeding into spending, and watch TSMC’s guidance as the definitive word on AI chip demand.

Friday, July 17: The week closes on housing and sentiment, with June housing starts and building permits at 8:30 a.m., industrial production at 9:15 a.m., and the preliminary July University of Michigan consumer sentiment plus its inflation expectations at 10:00 a.m. That last one matters most this week because the Fed is obsessed with inflation, the market will read the UMich inflation expectations line closely for any sign that consumers are bracing for higher prices.

Next week the earnings season broadens out of the banks and into mega-cap tech, and the market gets its first clean look at whether this week’s CPI actually changed the September hike math.

📈 Market Update

The market put in a daily and weekly hammer leaving us only about half a percent away from ATH. Another clear rotation has begun with weakness in chips like INTC 0.00%↑ and other names that have been leaders: AAOI 0.00%↑, GLW 0.00%↑ and QCOM 0.00%↑.

From here, we’ve seen MAGS 0.00%↑ push up with a lot of buying pressure. This could be the moment of the year where large caps finally participate in the rally. A perfect two week window for an earnings run up.

Tech still a little bit of a lagger, but shows the potential for the next leg up. Ideally, we want tech to lead so there’s a lot of catch up to do. If this does happen, we should get a large breadth move with a lot of participation.

Bitcoin:

Price is trying to establish a bottom here, but there is still a lot of work to be done. We will keep DCA’ing slowly with a timeline of around end of next year 2027 as take profit zone. This is about 12-18 months before the 2028 halving, which has historically been the peak.

🔍 What I’m Watching

5 names on the watchlist this week:

Strong bounce off the weekly 21 sending price right back to test ATH

Along with META 0.00%↑, these two of the MAG7 are leading the charge for the large cap tech rally.

It’s been a while but we’re starting to see AAPL 0.00%↑ move with the market instead of against it now. This to me is first signs of a character change + highest weekly close ever.

We can push to price discovery here quick before ER.

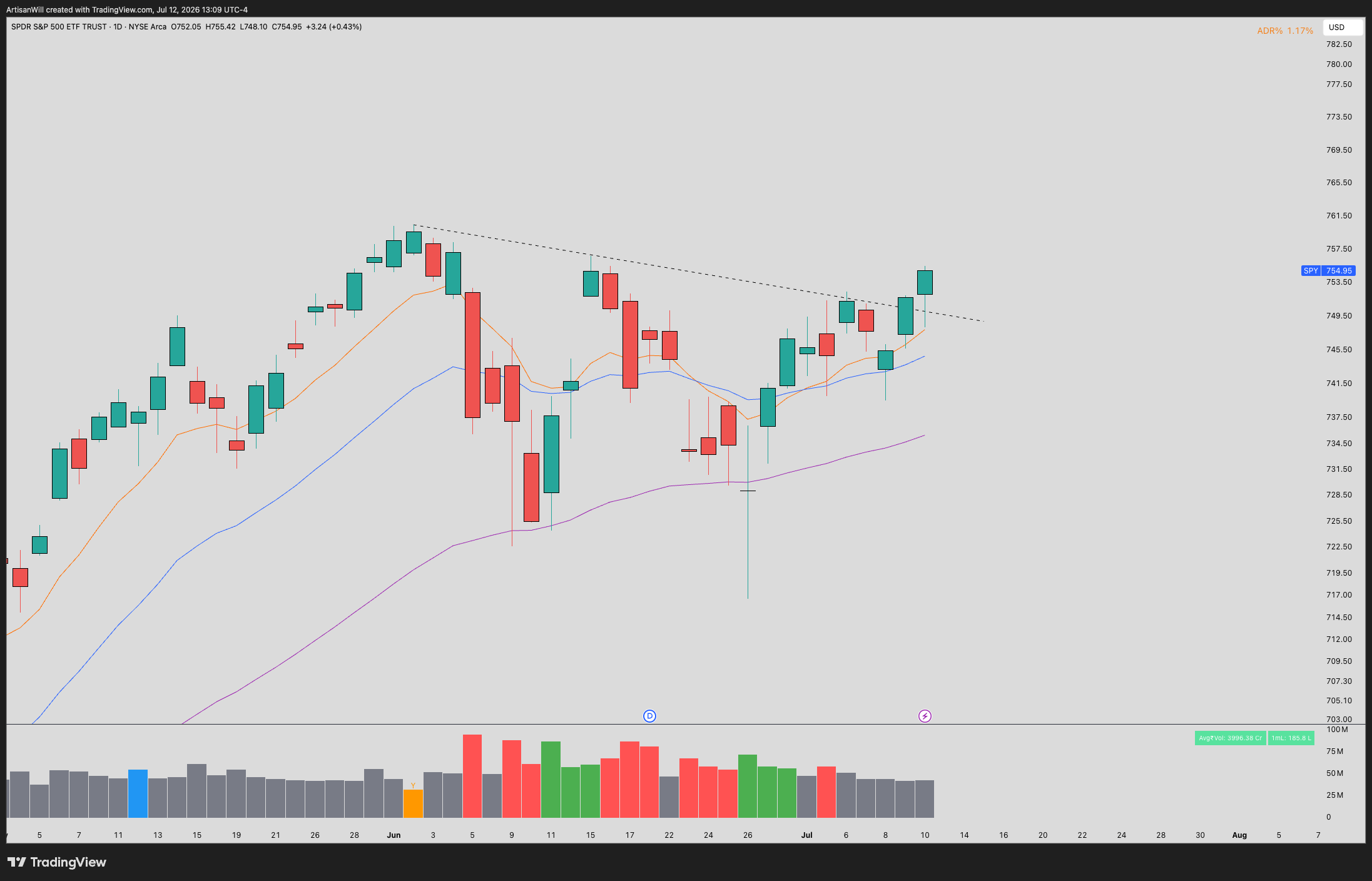

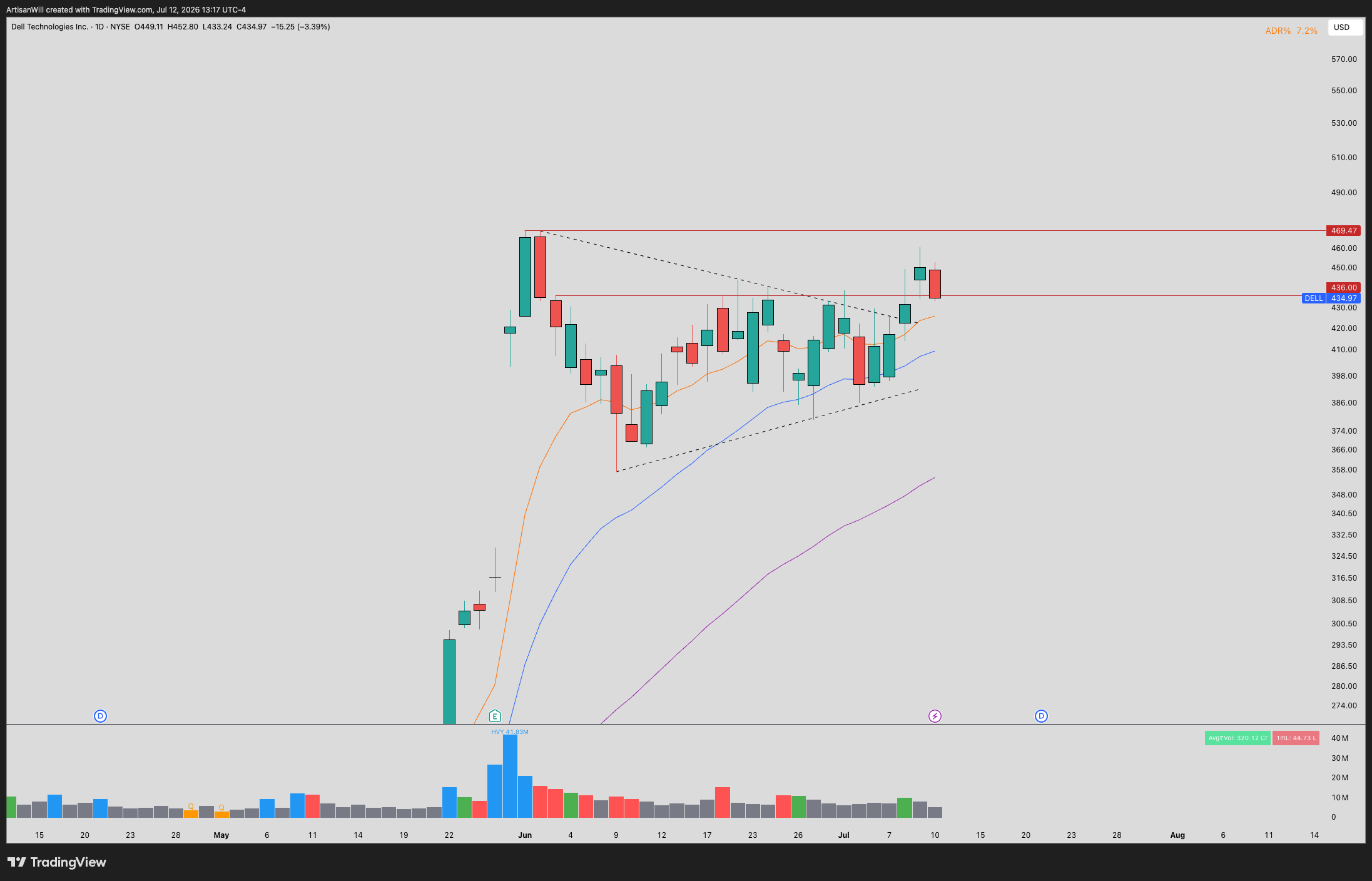

Weekly ended up closing under the 436 level

Seeing how there is some rotation out previous leaders, I would not be surprised if we can get another daily 21EMA tap for entry

This consolidation may continue for a couple more weeks before the next pop up

Large 600+ day monthly base over this 50 level

If price can push past again, this will be attempt number three at a breakout

Despite rising competition, enterprise platform growth is creating positive growth for the company.

If we can get past this 50 level, looking for 55+

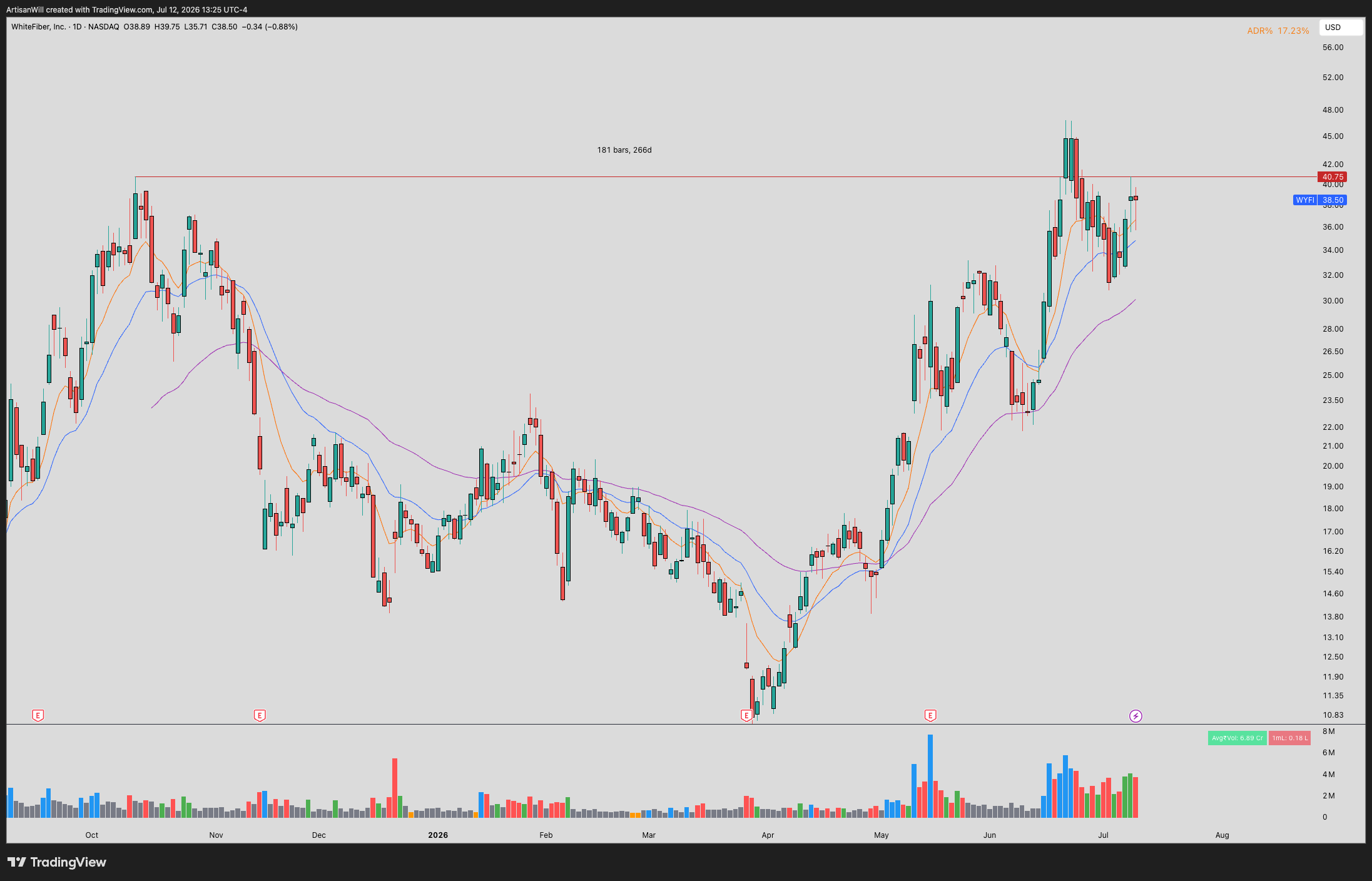

another massive weekly base with huge volume spikes at the right side

two indecision daily candles to close off previous week right under 40.75

daily close above this will be giving this breakout another shot, which opens the door to 50+

huge weekly curl that has taken a year to cook up

consumers keep spending on debt and SEZL 0.00%↑ is a clear benefactor of this behavior

price may require some consolidation here but sets up for a nice opportunity if 186.75 is broken

💡 My Take

The instinct into a week like this is to have a strong opinion about the CPI number and position for it. I would resist that. The market has already done most of the repricing work, moving from cuts to a 70% chance of a September hike, which means a lot of the hawkish outcome is in the price already. Betting hard on the exact print is a coin flip dressed up as analysis, and the tape has a habit of punishing people who confuse a forecast with an edge.

What I am actually doing is respecting the trend while sizing for the tail. The large cap trend is up and the records are real, so I am not fighting it. But the leadership is narrow, which has been the theme this year AND global tensions are still possible. That is a market that can keep working right up until it doesn’t, so this is a week to keep position sizes honest and to let the reaction to CPI and Warsh define the range before adding risk.

Concretely, that means watching how price behaves in the hour after the CPI release rather than trading the print itself, keeping an eye on the 10 year as the real tell, and treating any hot core reading paired with a hawkish Warsh as a signal to defend rather than a dip to buy. If the data comes in soft and the small caps finally join, that is a cleaner tape to lean into. Until then, patience is a position.

See you next week. Trade well.

Will